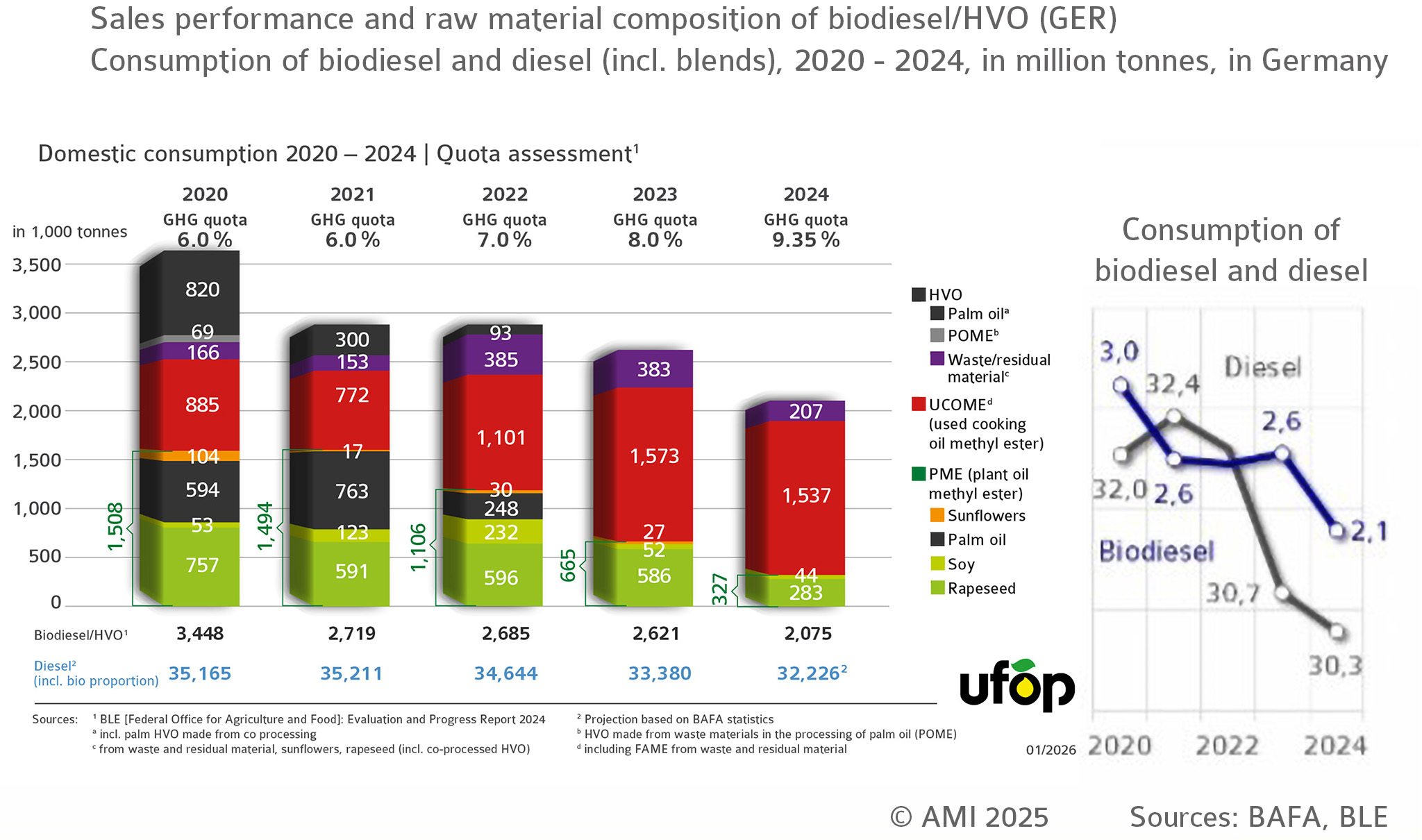

2.4.1 Feedstock composition influences consumption of biodiesel

According to information from the Federal Office for Agriculture and Food (BLE), just over 3.6 million tonnes of biofuels (previous year: 3.9 million tonnes) were marketed in 2024 and were counted towards greenhouse gas (GHG) reduction requirements. Of this, approximately 2.075 million tonnes were diesel-replacing biofuels (biodiesel and HVO), a significant decrease from the previous year (2.621 million tonnes). The drop was due to the high share (82 per cent) of biofuels derived from waste oils and fats. The benefit of these feedstocks is that they are included in the GHG balance calculation with a GHG value of 0 g CO2. Depending on the price, the high GHG saving performance makes these feedstocks ideal for mineral oil companies that are subject to quota obligations. The shares of biofuels from rapeseed oil and soybean oil decreased accordingly to approximately 15 per cent and about 2 per cent respectively.

In the quota year 2024, the share of HVO fell sharply, declining to 46 per cent. HVO is more expensive than biodiesel from waste oils. Biodiesel is preferentially used as long as the blending limit of 7 per cent by volume specified in the DIN EN 590 diesel standard is not exceeded.

The high total amount in 2020 was due to the fact that the 6 per cent greenhouse gas cap was met exclusively through the physical use of biofuels that year. GHG quota carryovers were permitted again as from 2021 – with the quota remaining unchanged. The option was discontinued again for 2025 and 2026. This means that the quotas can only be met with certificates obtained within the same year.

The average GHG reduction of 84%